Blockchain Can’t Stop Indian Bank Frauds?

The recent bank scams are surely not helping the common man to have a good night sleep. However, with the growing focus on digitization of backend processes and the buzz around blockchain, would the banks’ accountability improve?

In February, when the Punjab National Bank (PNB) scam came to light, most cribbed about another businessman (Nirav Modi) looting the tax-payers money through one of the most trusted financial institutions. This was not the first time. In the past too, similar scams had happened and hardly any lessons were learned.

In fact, according to the Reserve Bank of India (RBI), over 23,000 cases of bank fraud, worth Rs 1 lakh crore, have been reported in last five years. Increase in the number of non-performing assets (NPAs) along with such fraud cases, raise serious concerns about the health of the industry. Is there a solution to it? Not yet. However, if the banks start minimizing human intervention in majority of their processes and improve accountability, it might bring in some

relief.

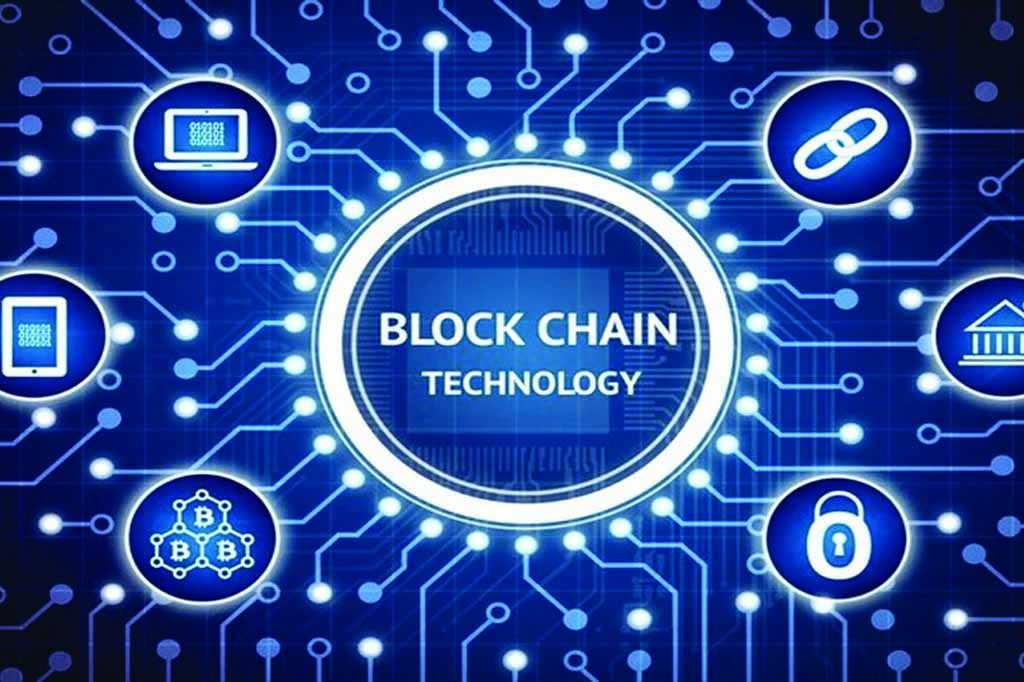

In the recent times, adopting blockchain is one of the best ways

through which the banks can improve their accountability. The technology enables trust to be formed between multiple stakeholders, by having data shared across a distributed ledger.

Giving an example, Chris Vincent, Project Manager, Elemential Labs, says, think about how Google sheets work as compared to the Excel. “In Excel, we have the opportunity to edit and then send it across via email, etc. This is very inefficient if multiple people are working on a particular file. On the other hand, Google sheet allows you to create a shared document that can be accessed and edited simultaneously by multiple stakeholders,” he shares, while adding, “This is what blockchain does for business problems that exist due to information being stored in silos. You could use this to create faster credit reports, reduce instances of fraud and solve a wide variety of problems.”

The Big Deal

The technology is believed to have a tremendous potential to solve issues related to banks, as several similar databases exist across organizations.

Santhosh Palavesh, Chief Innovations Officer, Belfrics Global, shares, “Suppliers, logistic companies, producers, retailers, insurance companies, banks, audit agents, everyone maintain their individual record, which create opportunities for fraudulent activities. Hence, financial institute, tax department are often puzzled with these records. If we can create a shared database, where every transaction can be authenticated by relevant participants, there will be appropriate access control and transactions will be more secure.”

It is difficult to imagine a world without banks; but, believe it or not, that’s where the world is headed. Chinmaya Sharma, Co-founder, Blockchain Semantics and Zeonlab, predicts, banks will resort to blockchain to negate chances of such frauds happening again, it is only a matter of time.

“Blockchain takes away all the administration access, maintains an audit trail of every transaction and ensures that the records once added can never be edited or deleted. If only loan certificates (or LoAs/LoUs) were issued on a blockchain platform, frauds like Nirav Modi-PNB would never have happened,” said Sharma.

He further elaborates, the rules of issuance of the letter of credit could have been coded in a smart contract and deployed on a blockchain platform, which cannot be changed after being deployed. Additionally, it would have been almost impossible to hide unauthorized certificates on the blockchain-enabled platform.

Where Are We Headed?

It is not just the blockchain companies that are singing its praises, globally even

banks are hopeful that the technology will help solve traditional processes, apart

from effectively managing and cancelling out NPAs and fraud cases. Nitin Chugh, Country Head – Digital Banking and Personal Liabilities, HDFC Bank, agrees that blockchain seems to be one of those technologies that can offer a better level of security and hence, it looks very promising. Furthermore, as against the popular belief that Indian banks are not ready for blockchain, Chugh says, “It has nothing to do with the existing IT infrastructure. The blockchain is going to be an entirely new infrastructure, as one would operate on a very different platform. So, the lack of it or presence of it will not change too many things.”

In line with HDFC Bank, even Kotak Mahindra Bank is quite optimistic. It feels, there is a lot of blockchain related opportunities, which will not just improve the time of trade but also save working capital, further improving the efficiency of the entire systematic architecture and enhancing the production cycle.

Before jumping on to blockchain bandwagon, banks need to address necessary issues related to technology, legality and most importantly mindset. “For blockchain to work, we would want banks, which generally work on multiple solutions, decide on a single system, at any given point. While on the other side, our laws need to evolve. Even though initiatives have been undertaken at the international level, it is equally important for countries like India to have laws in place,” shares Shekhar Bhandari, Senior Executive Vice President and Business Head – Global Transaction Services and Precious Metals.

While on the other side, Indian regulators, who are generally conservative in nature, are also taking cognizant of technological transformations coming in. Even the RBI is working with the consortium of banks along with Infosys-led Edgeverve to understand how blockchain can be implemented in securities and trade finance verticals.As most of the banks are working on their pilot project, in a year or may be two, we’ll see some major adoption. Sudin Baraokar, Head- Innovation, State Bank of India, says, by 2030, traditional bank services could cease to exist. So, the banks that will try to resist the technology will eventually fall out.

Source:https://www.entrepreneur.com/article/314911